TL;DR

Most travel agencies that hit a growth plateau look outward first; more ad spend, better creative, a new channel. The problem is almost never there. When traffic grows but revenue does not, when average booking value stays flat in a market where margins are already under pressure, or when your best people spend peak season firefighting instead of selling, the booking engine is almost always where growth has stalled. This guide gives OTA managers and agency owners the 10 revenue-visible signs to look for and what each one is actually telling you.

At some point, every OTA owner has the same conversation with themselves. The traffic numbers look good. The pipeline is active. The team is working. But the revenue line is not moving the way everything else suggests it should. The first instinct is to look outward ; more spend, better targeting, a new acquisition channel. And six months later, nothing has changed, because the problem was never upstream of the booking. It was inside it.

According to Skift Research’s March 2026 global OTA market estimates, the OTA market is projected to reach $107 billion by 2026, growing at a steady 7%. That growth is available to every agency in this market. The ones not capturing it are rarely losing to better marketing. They are losing to better infrastructure.

What Is Booking Engine Software and When Does It Become a Growth Constraint?

Booking engine software is the technology layer that connects a travel agency’s sales channels to live supplier inventory automating search, pricing, payment, and confirmation in real time, without a staff member in the middle of every transaction.

It is not a support tool. It is the commercial engine through which an OTA competes. And like any engine, it has a working range. The business that has grown past that range is not facing a marketing problem or a pricing problem. It is running at full load on a platform built for a smaller version of itself.

Key Terms Worth Knowing

Booking Engine Software : The technology layer automating search, pricing, payment, and confirmation between a travel agency’s sales channels and live supplier inventory in real time.

Look-to-Book Ratio : The number of availability searches made for every confirmed booking; a declining ratio indicates pricing gaps, checkout friction, or inventory unavailability inside the engine

Mobile-First Architecture: A booking engine designed from the ground up for touch navigation and fast mobile load times, as distinct from a mobile-responsive design that adapts a desktop interface.

B2B Sub-Agent Portal : A branded, access-controlled section of a booking engine that allows partner agents to search, book, and manage inventory at pre-agreed rates with independent markup controls per tier.

How Does Failing Booking Engine Software Destroy Conversions You Have Already Paid to Earn?

Here is what rarely appears in a marketing report: the cost of traffic that arrives ready to book and leaves without completing a transaction.

Ad spend gets attributed to clicks and sessions. What it rarely gets attributed to is the checkout experience those sessions land in. Every traveller who searched, compared, entered their details, and then abandoned , that is a cost the acquisition budget absorbed and the booking engine failed to convert.

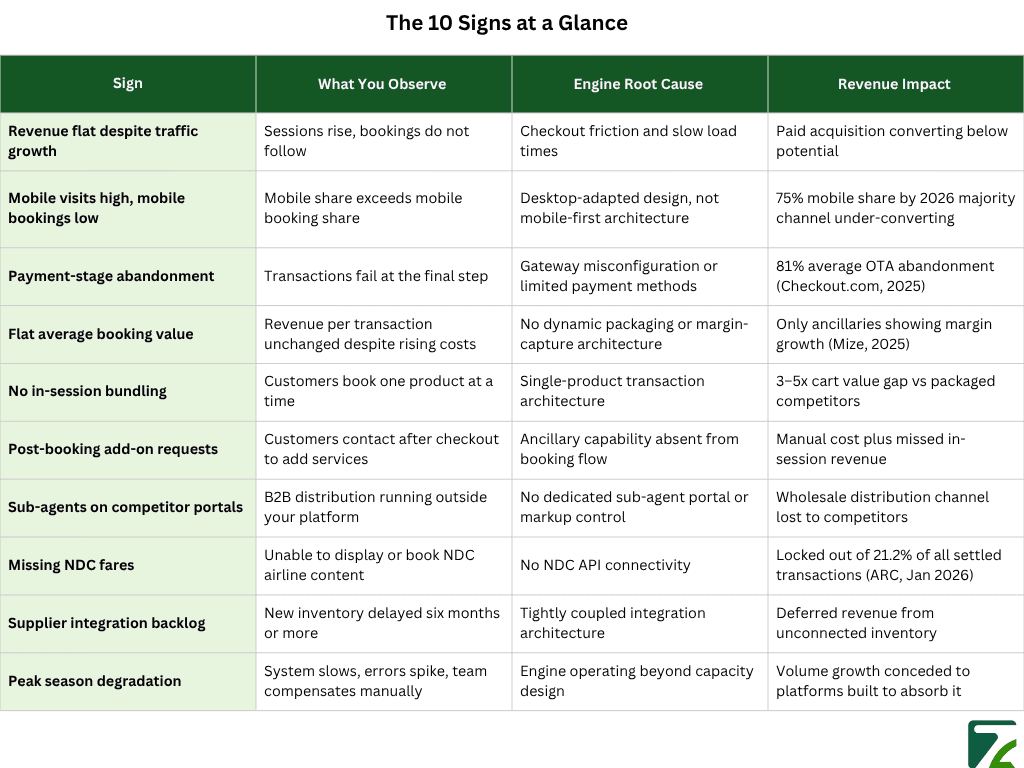

Sign 1: Why Does Revenue Stay Flat When Your Booking Engine Software Is Seeing More Traffic?

Traffic growing and revenue not following is a specific kind of problem. It tells you the demand is there. Travellers are arriving with intent. Something inside the journey is breaking that intent before it becomes a booking.

Contentsquare’s 2026 industry analysis found that travel and hospitality sites convert at just 2.7% on average and on mobile, that drops to 2.1% against 4.5% on desktop. The gap is not random variation. It is the measurable cost of friction that should not exist: slow search results, pricing that has not refreshed since the traveller started browsing, a checkout flow with one unnecessary step built into it.

None of this shows up in a paid media dashboard. All of it shows up in the distance between sessions and confirmed revenue. When those two numbers are pulling in different directions, the checkout architecture is almost always where the answer is found.

An agency that pays to acquire traffic and then loses it inside a broken checkout is not facing a marketing efficiency problem it is funding a leaking bucket.

Sign 2: Why Are Mobile Visitors Converting at Half the Rate of Desktop Users?

Prostay’s January 2026 hotel booking statistics report projects mobile-first booking at 75% of all OTA transactions by 2026. For most agencies, mobile is no longer a secondary channel. It is the channel.

There is a meaningful commercial difference between a mobile-responsive booking engine and a mobile-first one. The first reshapes a desktop experience for a smaller screen. The second was built for a traveller navigating with their thumb, on a connection that is not always fast, in a moment that is not always patient. When that traveller hits a checkout designed for desktop, they do not complain. They leave and that departure costs the agency the full value of everything that brought them there.

Sign 3: Why Do More Bookings Fail at Payment Than at Any Earlier Stage of the Flow?

Sign 3: Why Do More Bookings Fail at Payment Than at Any Earlier Stage of the Flow?

This is the one that stings the most because the traveller was committed. They searched, compared, selected, and entered their details. Then something in the payment layer broke the transaction.

Checkout.com’s 2025 payments performance research puts average cart abandonment across OTA platforms at approximately 81%. A disproportionate share of that happens at payment , not because travellers changed their minds, but because the engine gave them no way to complete. A fraud filter that rejected a legitimate card. A redirect to an unfamiliar processor. A payment method the traveller uses every day that the platform simply did not offer.

Every one of those is a recoverable failure. None of them are being recovered if the engine does not surface them. The agencies capturing the growth in this market are the ones whose platforms close what their marketing opens.

What Revenue Is Your Booking Engine Software Leaving Behind on Every Transaction It Processes?

The conversion problem shows up in traffic-to-booking ratios. The revenue-per-booking problem is quieter it accumulates one transaction at a time, each processed at less than its full value, because the engine was never designed to capture the rest.

Sign 4: Why Has Your Average Booking Value Not Moved Despite Rising Travel Costs Across Every Market?

This is the 2026 version of a problem that has been building for three years. Booking volumes have recovered. Travel costs have risen. But OTA margins are not recovering at the same pace.

According to Mize’s December 2025 travel industry recovery analysis, Expedia’s EBITDA margin compressed from 25.9% in 2019 to just 9.9% while ancillary revenue remains the only booking vertical where margins are actively growing. The same report is direct about what this means: growth in the current environment means shifting from volume to margin expansion. An engine that processes every booking as a standalone product sale no upsell, no packaging, no ancillary capture is positioned for exactly the wrong side of that shift.

When suppliers earn more per booking through fare increases and the agency’s margin does not follow, that is not a negotiation problem. It is a platform architecture problem, compounding silently with every confirmed transaction.

Sign 5: What Does Your Agency Lose When an Online Booking Engine Cannot Bundle Products in One Transaction?

61% of travellers choose OTAs specifically to book bundled flight and hotel packages, according to Navan’s 2025 travel booking research. That majority is not looking for the cheapest standalone flight. They are looking for a complete trip priced, confirmed, and paid in one place.

When the platform cannot deliver that, Switchfly’s December 2025 research shows exactly what happens: packaged trips generate 3 to 5 times the cart value of standalone bookings. That multiplier is available on every qualifying transaction. An engine without dynamic packaging capability is not missing a feature. It is processing the majority of its highest-value booking demand at the lowest possible margin every day, without a record of what was missed.

An engine without dynamic packaging capability does not miss upsell moments. It processes every transaction at its lowest possible value permanently, and invisibly.

Sign 6: Why Are Post-Booking Add-On Requests Still Arriving by Phone and Email?

Pay attention to what customers request after they book. Transfers they could not add during checkout. Insurance that was not offered in the flow. An upgrade requested by email the next morning. Each of those requests tells the same story: the traveller had intent to spend more, the engine had no mechanism to capture it, and the request arrived in an inbox to be handled manually at a fraction of the efficiency it should have required. This is not a customer service observation. It is a revenue architecture diagnosis.

Which Booking Engine Software Gaps Are Quietly Redirecting B2B and NDC Revenue to Competitors?

Leisure bookings test an engine’s conversion flow. B2B distribution and airline content access test its structural depth. This is where most mid-market booking engine software quietly fails and where the consequences extend beyond a single lost transaction to an entire distribution channel running on a competitor’s platform.

Sign 7: Why Are Your Sub-Agents Booking Through Competitor Platforms Instead of Your Own System?

Sub-agents are the distribution multiplier for any wholesale OTA or DMC. Every sub-agent booking through a competitor’s portal instead of yours is not a lost transaction. It is a lost relationship, executing volume on someone else’s platform building someone else’s data, someone else’s reconciliation trail, and someone else’s network effect.

The reason sub-agents migrate is rarely price. It is friction. When your platform requires them to call for availability, email for confirmation, and wait for manual markup approvals, a competitor offering instant self-service access wins the relationship by default. According to Expedia Group’s Q1 2025 results reported by Protect Group, B2B gross bookings grew 17% year-over-year, the strongest segment in Expedia’s entire portfolio. The agencies winning that growth are the ones whose booking engine software supports B2B distribution natively, not through workarounds.

A platform without dedicated sub-agent logins, per-tier markup controls, and real-time inventory access is not failing at a feature. It is absent from the fastest-growing distribution channel in the current OTA market.

Sign 8: What Airline Fares Is Your Best Online Booking System Currently Unable to Display?

According to the Airlines Reporting Corporation, via Travel Weekly, January 2026, NDC accounted for 21.2% of all settled airline transactions in December 2025 ,up from 20.3% twelve months earlier. Airlines including Lufthansa, British Airways, and Air France-KLM are concentrating their best fares and promotional inventory inside NDC channels.

An agency whose best online booking system has no NDC connectivity is selling from an incomplete shelf. The fares its competitors are displaying today are sitting in a content layer the engine cannot access and the agency has no visibility into exactly what it is missing.

Sign 9: Why Does Adding a New Supplier to Your Booking Engine Software Take Months Instead of Days?

When a new supplier partnership is agreed, the conversation turns almost immediately to the integration timeline. For agencies running on legacy or tightly coupled architecture, that timeline is measured in quarters , not days. A well-built booking engine treats supplier connectivity as configuration. A poorly built one treats it as construction. Every month a supplier sits unconnected is a month of inventory the platform cannot sell. When pending integrations grow faster than completed ones, that list is not a backlog. It is a structural limit made visible on a spreadsheet.

What Does Peak Season Actually Reveal About the Real Limits of Your Booking Engine Software?

Peak season does not create problems. It exposes them.

The performance wall a booking engine carries all year becomes unmistakable when demand doubles. What the team managed through workarounds in February becomes unmanageable in July. What felt like occasional friction becomes a daily operational crisis the entire team absorbs often without the leadership level ever seeing it clearly.

Sign 10: Why Does Your Booking Engine Software Slow Down at the Exact Moment Your Business Needs It Most?

Search results slow. Pricing falls behind live rates. Booking confirmations delay. Supplier sync errors multiply. And the operations team does what experienced travel operations teams always do they compensate. They call suppliers directly. They re-verify manually. They fix errors by hand before the customer notices.

The bookings confirm. The customer experience is preserved, mostly. And at the leadership level, peak season looks like a success intense, but managed.

What it actually was: a demonstration of the exact volume at which the engine runs out of capacity. The volume at which a booking engine performs reliably is the volume at which the business can grow. If peak season is already hitting that wall, the agency is not managing a seasonal spike, it is bumping against a constraint that will be waiting next year, at the same point, for the same reasons. Every season where the team compensates manually is a season where the agency’s scale is being set not by the market, but by its own infrastructure. According to Skift Research, the OTA market is heading toward $107 billion by 2026. That growth does not wait for platforms to catch up.

The 10 signs in this guide share one diagnosis. Flat conversion. Stagnant booking value. Sub-agents on competitors’ platforms. A team that dreads peak season. These are not separate problems, they are the same platform, showing its limits in different parts of the business, at different times of the year. The question is not whether it is constraining growth. It is how long it already has been.

Assess your current platform against these 10 signs and identify which gaps are already visible in your revenue data. The earlier the diagnosis, the lower the cost of the correction.

Conclusion

The agencies growing through this market are not running better campaigns than their competitors. They are running better infrastructure , platforms built to close what marketing opens, capture the full value of every transaction, and hold performance under the demand the business actually generates. Every sign in this guide has a fixable cause, and the earlier it is found, the less it costs to correct.

Frequently Asked Questions

Run a session-to-booking funnel report segmented by device and broken down by checkout stage. If mobile conversion sits more than 2 percentage points below desktop, or if payment-stage abandonment exceeds 40%, the engine's checkout architecture is the variable to investigat not campaign performance or pricing strategy.

Top-performing booking engines for leisure OTAs deliver conversion rates between 3% and 6%, with mobile-first platforms narrowing the desktop gap significantly. A persistent rate below 2.5% on mobile or below 3% overall is not a market benchmark to accept. It is an engine performance threshold with a fixable cause.

Discounts reduce the margin on a transaction already in process. Dynamic packaging increases the total value of the transaction before it begins. Packaged trips generate 3 to 5 times the cart value of standalone bookings, according to Switchfly's December 2025 research, a multiplier that no discount strategy replicates across a full booking cycle.

When the compounded cost of workarounds manual processing time, delayed supplier onboarding, sub-agents migrating to competitor platforms, and team capacity spent compensating for platform limits exceeds the cost and disruption of migration, the engine has moved from an optimisation problem to a structural one.

At minimum: individual sub-agent logins with role-based permissions, per-agent markup and commission control, real-time inventory with instant confirmation, a white-label branded portal experience, and a reconciliation layer that tracks agent performance and outstanding balances automatically. An engine without these cannot scale a wholesale distribution channel.